Prices started rising as COVID rocked global supply chains in 2020 and 2021 and haven’t yet returned from the stratosphere.

Back in the pandemic’s early days, when car dealerships started looking more like vacant lots, paying over MSRP was more common than ever. In fact, it wasn’t unusual to buy a car and then, several months later, realize it had actually increased in market value. While those days are gone, the high prices and inflated interest rates live on. And there’s little to suggest it’s getting better any time soon.

Brandon Bell/Getty Images

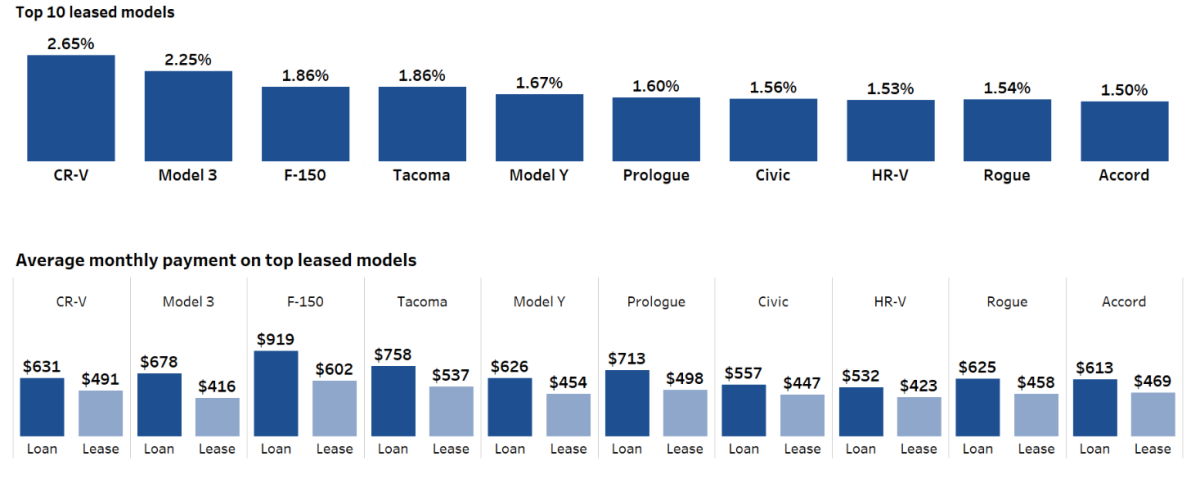

Over the last five years, vehicle pricing has soared

You don’t need to look hard to find evidence that cars are more expensive than ever. New car average transaction prices are now around $10,000 higher than pre-pandemic pricing, according to KBB. To illustrate that fact, consider Ford. Between this year and last, Ford’s average transaction price has increased to $54,082 from $53,786. But, more illuminating, that’s up from $46,070 in January of 2021. Surprisingly, that undercuts the average transaction price across all cars sold, which sits at $48,039—and yes, that’s an increase of 1% year over year. It was under $40,000 in 2020, according to KBB. The anomaly isn’t limited to just new vehicles, either. Used listing prices throughout 2024 were down slightly compared to the year before, according to Cox Automotive. But at $25,467, it still marks a 32% increase over where prices were in 2019.

Consistent rate increases have helped contribute to astronomical payments

Let’s continue to stick with the Ford example. Since late 2022, the average Ford F-150 finance payment has floated around $900, occasionally dipping just below that number and hitting a high of $983. As with all auto loans and leases, only part of that comes down to transaction price; the other half is interest rates. Rates have been on the rise since 2022, when the Federal Reserve began a series of 11 rate increases before holding steady at 5.25% for 14 months. While rates have eased—very slightly—since, a quick look at interest rates across new and used vehicles is sobering.

According to Edmunds, the average new car APR in some areas of the US, like New Mexico, is as high as 8.78%. The lowest state average is hardly “low,” sitting at 5.58% in Minnesota. Used car interest rates paint an even bleaker picture. Across the country, averages are well into the double digits. The lowest average is 8.93% in Vermont. The state with the highest average used car loan rate in February was Mississippi, at a legitimately heart- and wallet-breaking 13.46%. Over half of US states have an average used car loan payment sitting at 10% APR or above.

Experian

Higher prices usually indicate a slowdown, but data suggests otherwise

As the data indicates, prices have been generally on the rise for a while now. But there’s simply no slowing down America’s appetite for expensive vehicles. Thanks to data compiled by Cox Automotive, we know that year over year, buyers are taking home more vehicles priced at $100,000 or more. In the first two months of 2025, automakers sold 52,000 units at six figures or more, dwarfing the 46,000 units recorded in the same time last year and crushing 2020’s figures of just 12,000. In fact, Cox initially projected yearly sales to remain almost identical from 2024 to 2025, around 16 million, although the organization has recently dropped that estimate to 15.6 million. This brings us to the next chapter.

Experian

Tariffs could slow down purchases—but prices won’t drop

Cox Automotive cites “affordability challenges, economic uncertainty impacting consumer confidence, and the potential for higher inflation due to new tariffs” as reasons for revising their sales outlook for 2025. But it’s important to note that the first data point has been around for nearly half a decade now, and the second one is purely subjective. The Trump administration’s tariffs, should they go into effect, will make every single vehicle more expensive. And when you factor in the record-high interest rates Americans are either oblivious to or willing to pay, it amounts to a vehicle getting thousands, not hundreds, of dollars more expensive. Even if automakers wanted to drop prices, it becomes much more difficult with what’s effectively a 25% tax rate being levied every time a component (or the vehicle) crosses a US port.

Final thoughts

Americans are paying more than ever for vehicles. In the process, many buyers are overextending on jacked-up car payments. And it’s telling; another Cox Automotive study reports car repossessions are at their highest level since 2009, and the number of defaults is even higher (2.3 million vs. 2.2 million). With only higher prices on the horizon, economists probably aren’t the only ones with the word “crash” materializing in their alphabet soup. Something will have to give, and it’s anyone’s guess whether consumers or OEMs will realize that first.

Leave a Reply